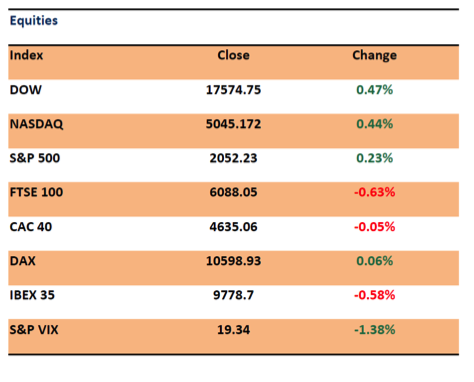

US Stocks rose yesterday but the FTSE fell for the seventh day in a row. The S&P 500 rose 0.23%

In overnight trading, almost all Asian indices are trading lower with the main exception being the Nikkei 225 which is up 0.97%. Chinese stocks fell after another executive of a major firm has gone missing. European indices are opening lower and the US futures currently indicate that US indices are set to open higher. The South African Rand weakened further yesterday to a new all time low and South African Bonds fell further as the market responded to the removal of the Finance Minister.

Oil fell further yesterday with the WTI currently trading at USD 36.66 per barrel, a new 11 year low.

Iron ore hit a new all-time low and these declines drove the Bloomberg Commodity Index lower and close to the all –time low seen in late 1998 as shown in the chart below.

Government bonds were relatively steady as US bonds yields rose while those in Europe fell. The 2 year treasury rose again to a new 4 year high as markets more fully price in a 25 bp interest rate increase by the Federal Reserve next week.

Credit spreads have widened over the week again as risk aversion continues to increase. The Xoverindex which measures the spread of BBB/ BBB- corporates in Europe rose to over 300 bps.

Currencies have been relatively stable in the last two days after recent high volatility and the general trend has been towards a slightly weaker dollar.

Outlook

In Europe today, we’ll get the final reading for German November CPI (with no change expected). In the UK, the latest construction output numbers are due.

In the US, the main focus will be on the retail sales data. The November PPI data as is the University of Michigan consumer sentiment number for December are due out.

There is an interest rate decision by the Russian Central Bank.

In general markets will be relatively quiet as we look ahead to the Federal Reserve Interest rate decision next week. Market prices suggest an over 80% probability of a 25bp increase (to 0.5%) in the Fed Funds rate. European stockmarkets are lower this morning and US stocks are currently expected to open higher later today.